Klarna Wants More Than Your Payments. It Wants Your Deposits.

For years, buy now, pay later (BNPL) providers have competed with banks at the point of purchase. Now they’re coming for deposits. Klarna recently launched a high-yield savings account in the U.S., adding another piece to its growing financial ecosystem. While the company isn’t a bank in the United States, it’s partnering with WebBank to offer FDIC-insured savings accounts with competitive interest rates. On the surface, it looks like another product launch. But it signals something much bigger.

The Goal Isn’t Just Savings

Klarna isn’t simply introducing a savings account, it’s creating more reasons for consumers to keep their money—and their financial lives—inside the Klarna ecosystem.

The more often consumers open the app to shop, save, spend, or borrow, the stronger that relationship becomes. That’s a trend banks and credit unions can’t afford to ignore.

What This Means for Financial Institutions

Consumers have more choices than ever when it comes to where they save, spend, and borrow.

Traditional banks are no longer competing only with other financial institutions. They’re competing with fintechs that are building everyday financial relationships through convenient digital experiences. That makes it even more important to understand customer behavior before deposits begin to move elsewhere.

Seeing the Signals Earlier

One of the earliest indicators of changing financial behavior can be found in transaction data. Customers who begin using BNPL providers more frequently may also be engaging with those providers in other ways, including savings products and additional financial services. Understanding those trends gives financial institutions an opportunity to respond before relationships begin to shift.

How IFM Can Help

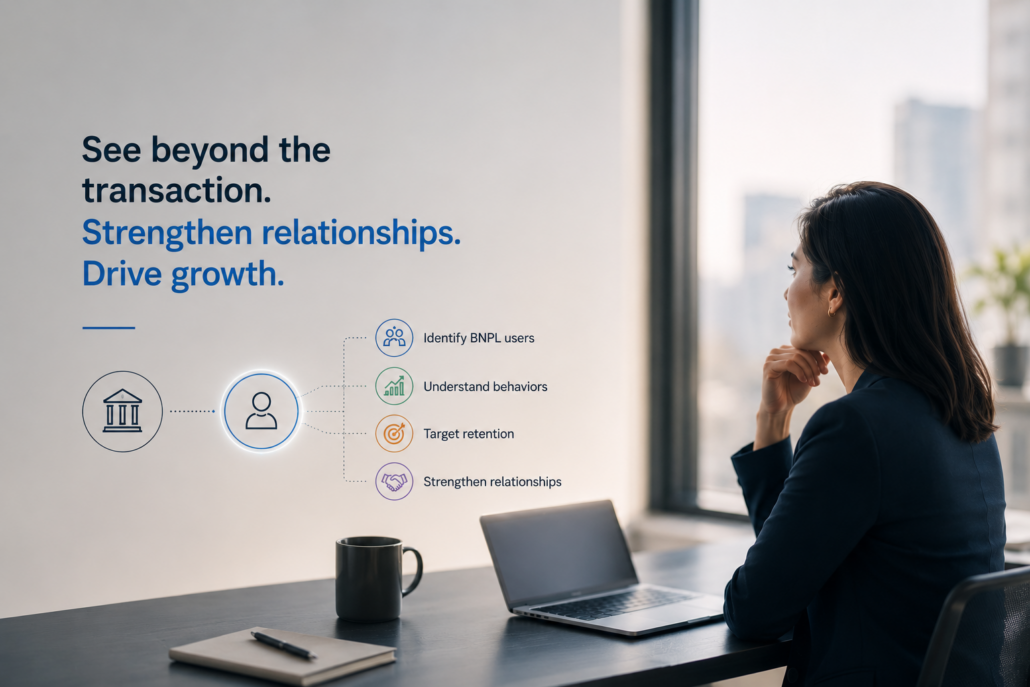

IFM provides merchant-level transaction reporting that helps financial institutions identify activity with BNPL providers like Klarna, Affirm, Afterpay, Sezzle, and others. Instead of seeing only a generic transaction, institutions gain deeper visibility into where customers are engaging with these providers.

That insight can help banks and credit unions:

- Identify customers actively using BNPL providers

- Understand emerging payment and savings behaviors

- Develop targeted retention campaigns

- Strengthen deposit relationships before competitors do

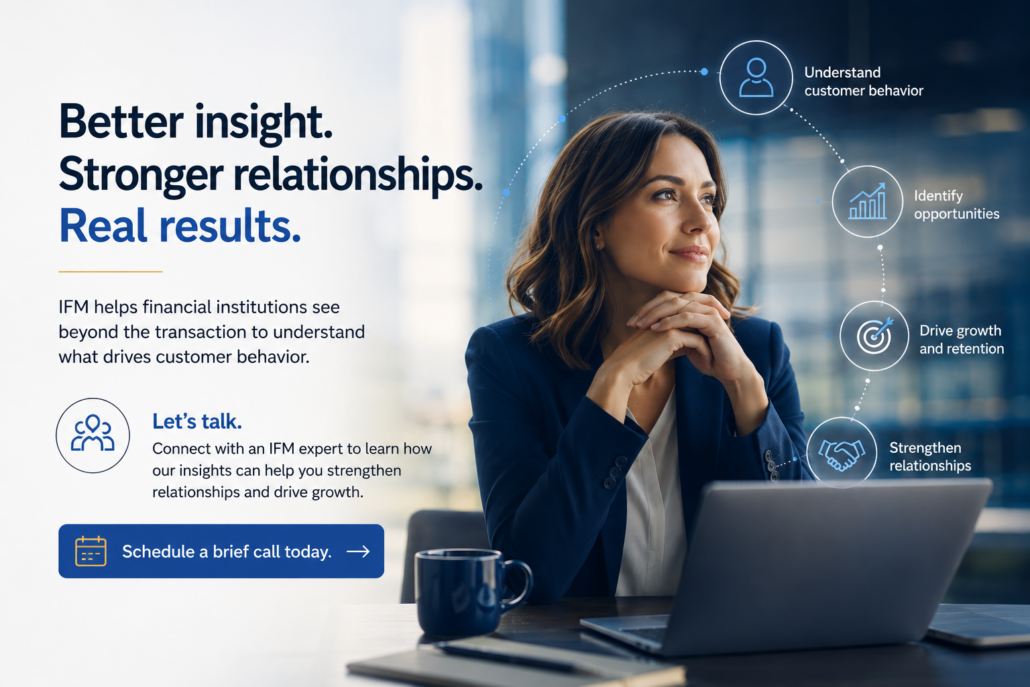

As fintechs continue expanding beyond payments and lending, understanding customer behavior becomes more important than ever.

The institutions that act on those insights won’t just respond to change—they’ll be better positioned to stay ahead of it.

Cassandra Magno is a Marketing and Business Development Coordinator at IFM. She specializes in process improvement, strategic planning, and partnership development, with experience helping organizations streamline operations and achieve their goals. Drawing on her analytical mindset and passion for problem-solving, Cassandra enjoys exploring industry trends and sharing insights that help businesses make informed decisions and drive positive results.